Quick Apply for Small Business Funding

APPLY FOR SMALL BUSINESS FUNDING

WHAT IS SMALL BUSINESS FUNDING?

Small business funding help provide much needed cash flow to keep companies up and running. Funding provided to small businesses for various purposes by First Down Funding. These funding may have less restrictive requirements, enabling the small business to secure the funds. A small business funding may provide other incentives for the borrower, which could minimize expenses for the business. The cost of working capital of small business owners looking for a funding might be on the decline, but they still borrow a lot: $600 billion each year.

Small business funding exist to help businesses succeed, but many times business owners get them for the wrong reasons, and problems they thought would be solved spiral out of control. … If your company is profitable and you have decent cash flow, but you need funds to expand, then a funding is a good idea.

DETERMINE YOUR NEED FOR SMALL BUSINESS FUNDING

There are a few variables to consider when determining the right small business funding for your company. Think about whether a long-term or short-term funding option is best for your needs. If you just need funding to fulfill a large order or take advantage of a one-time opportunity, funding with shorter terms is probably best. If you need to purchase a piece of machinery that will last 20+ years, long-term funding is more cost-effective.

HERE ARE 5 REASONS WHY YOUR BUSINESS MIGHT NEED A FUNDING:

Inventory

Cash Flow

Equipment

To Improve Terms on a Larger Funding

Expansion*

*Probably the most obvious reason to consider small business funding is to invest in an expansion opportunity for your business.

Learn more about what your business qualifies for with First Down Funding.

WHICH BUSINESS FUNDING TYPE FITS YOUR NEEDS?

ARE YOU LOOKING FOR SMALL BUSINESS FUNDING?

Speak to one of our qualified and seasoned Small Business Funding Managers to better understand what funding options and approvals we have for your small business.

APPLY NOW WITH FIRST DOWN FUNDINGCALCULATE A DESIRED SMALL BUSINESS FUNDING PAYMENT

One of the most important things to determine before applying for small business funding is how much you can afford to pay back on a monthly basis. Don’t be too ambitious when making this calculation in order to avoid defaulting and causing damage to your credit history.

You should determine exactly how much your business needs to borrow to achieve its goals. This should be a precise figure, not a range. Funding companies want to see that you’ve done your research and that you will spend their money in a way that will help your business thrive. They want you to succeed so they’re sure to get paid back.

ARE YOU CREDIT WORTHY OF SMALL BUSINESS FUNDING

CHECK YOUR CREDIT HISTORY

To be considered creditworthy, borrowers must provide First Down Funding with adequate financial information to prove their ability to payback the funding.

IDEAL CREDIT SCORE FOR A FUNDING

Borrowers should expect to have good credit to qualify for business funding. Funding partners build an assessment of the applicant’s character by evaluating how they handled debt in the past.

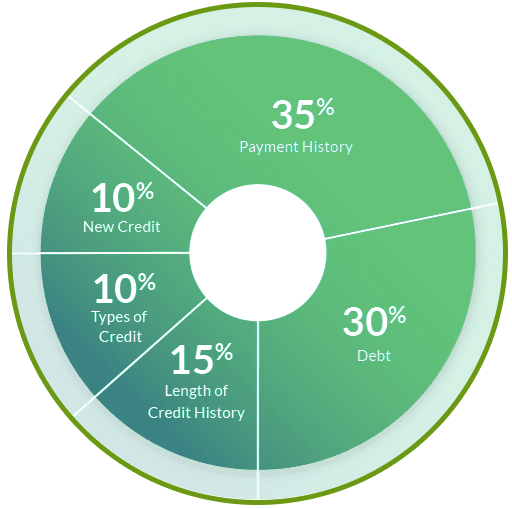

CREDIT SCORES ARE BROKEN DOWN

FICO Scores are comprised of payment history (35 percent), types of credit (10 percent), debt (30 percent), new credit (10 percent), and length of credit history (15 percent). The history reveals the borrower’s ability to pay on time on their installment funding, credit cards, finance company accounts, and mortgages. Potential show stoppers include bankruptcies, excessive credit inquiries, liens, foreclosures, lawsuits, and judgments.

HOW TO PREPARE FOR SMALL BUSINESS FUNDING:

Here are five steps to help you qualify for small-business funding.

- Build credit scores.

- Know the First Down Funding qualifications and requirements.

- Gather financial and legal documents.

- Develop a strong business plan.

- Provide collateral.

The ability to pay back the funding based on collateral, financial reserves, and assets.

The borrower’s successful past performance in business (for a new business)

The borrower’s existing cash flow (for an existing business)